by Mark Burnam

When you retire and begin your "second half of life", work because you want to, not because you have to. Isn't that what you want? In our previous articles, we talked about the four basic steps to securing a more sound retirement, including decisions for workers 5 to 8 years out, and issues for those in already in DROP and close to actual retirement. In this article we wish to touch upon the effect of inflation in regard to one's pension income with or without a Cost of Living Adjustment (COLA).

When you retire your pension income will either be fixed or have an annual "cost of living adjustment" more commonly known as a COLA. They come in many forms from 1% - 3% a year for life, to staggered, to vanishing after a certain amount of years, to none at all. Most of the folks we work with in the Florida Retirement System (FRS) are enjoying a 3% COLA and we are now seeing a slightly reduced COLA i.e. 2.85% 2.65% and so forth for those retiring in the next few years. Their reduced COLA calculation depends upon length of service, when they entered DROP, retired, and so forth. The folks we work with in various city pension plans are all over the map in regard to COLA's as some have them and others have had their COLA's reduced or completely eliminated. It is what it is.

Let's address the "elephant in the room" before we get started. Some pensions have COLA's and some don't. While it is a hot topic and sore subject for many, it is what it is so let's deal with the facts as they are. The upside? Fortunately, you have a pension, a DROP, perhaps some moneys saved in a 457 account, or more. If you have no COLA, then your DROP and other investment assets need to BE your de facto COLA -> they may need to be strategically positioned and invested differently to combat the inflationary effects on one's pension by providing you a rising income (either currently or in the future when you need more income).

Let's address the "elephant in the room" before we get started. Some pensions have COLA's and some don't. While it is a hot topic and sore subject for many, it is what it is so let's deal with the facts as they are. The upside? Fortunately, you have a pension, a DROP, perhaps some moneys saved in a 457 account, or more. If you have no COLA, then your DROP and other investment assets need to BE your de facto COLA -> they may need to be strategically positioned and invested differently to combat the inflationary effects on one's pension by providing you a rising income (either currently or in the future when you need more income).

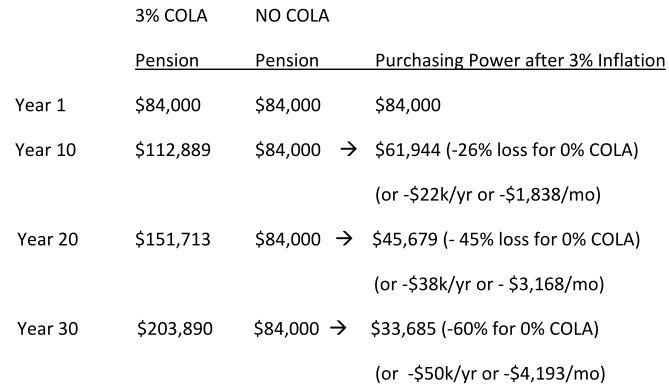

In our previous articles we had a DROP retiree retiring with an income of $7,000/mo(or $84,000/yr.), a DROP account of $400,000, and a 457 deferred comp plan value of $150,000. Let's take a look at two different pensioners: one with a 3% COLA and one with 0% COLA and the effects of inflation and no COLA:

Bottom line, with most of our first responders retiring in their mid-50's (give or take) coupled with longer life expectancies, you can see the devastating effects inflation can have on ones purchasing power over time. So what is one to do?

Let's also take a look at one's annual living expenses. If you had an $84,000/yr pension and your annual living expenses were $50,000 when you retired -> in year 10 your pension is still $84,000, but your expenses grew at 3% a year and are now $67,195 in real terms and in 20 years they will be $90,304! You're under water and this just assumes 3%. Healthcare, college costs, and more are all growing 5 - 7%/year, or more. Gulp!

So how does this all translate to you now? Fact: you may need to start withdrawing moneys from your DROP/other retirement accounts to fund your retirement. How much? When? For how long? Can you afford to invest all your moneys in some guaranteed fixed 3.5% rate account? Can you afford to earn only 5%? Other? Will you risk depleting your DROP/other retirement accounts with that approach at some point in your life? If so, what then?

We sometimes tend to see what is right in front of us and some folks we meet with just shrug and hope things will work out down the road. In our practice, we don't want to "wing it" with your "second half of life" financial future and just "hope things work out" for you. We want any surprises in retirement to be positive surprises so we plan accordingly. How? We "stress test" your plan by running assumptions with conservative/understated investment returns and beefed up/rainy day expenses rising at more than 3%. If your plan looks good under those conditions then you should be in great shape. If not, then it will show up under the investment return you actually need on your DROP and other assets to ensure you don't deplete these assets. Is it 3%? 5%? 7%? 9%? More? The lower return you need to earn on those assets the more options you have and the more conservative you can be. Your jobs were stressful enough all those years; do you really want to HAVE to earn over 9% a year to fund your retirement expenses and to NOT deplete your assets? Clearly not.

No Worries Plan

So, let me say it again, while your pension should always be there, running out of money i.e. depleting your retirement assets can be a possibility for some folks if not planned for and addressed ahead of time– not after the fact.

So, let me say it again, while your pension should always be there, running out of money i.e. depleting your retirement assets can be a possibility for some folks if not planned for and addressed ahead of time– not after the fact.

And the lack of a COLA is not necessarily always the biggest culprit. Sometimes it is you! It doesn't have to be, but we all know people who have blown their DROP by taking pre-mature distributions (withdrawals) without any thought or concern to the tax implications or future needs. They (or their "advisor") didn't know or give proper guidance in respect to which accounts and assets to withdraw from first. Pre-50, 55, and 59 ½ rules are important considerations and working with someone who knows these rules is a must.

Big Worries

Smart vs. not so smart? -> taking money out of your DROP to buy that RV, paying off a mortgage or other debt, buying that fancy car, toy, whatever, not to mention divorces, quadros, IRS issues, and the list goes on and on to even no reason other than they just wanted the money in their hands so to say. And, realistically you may want to or need to work a second career for a while to pay for healthcare costs or until Social Security kicks in etc. All these are addressed in your plan. The battle between "Wants and Needs" is often difficult. Can you afford to do those things without seriously risking putting a major dent in your financial security and future? We plan for them ahead of time and sometimes the answer is a resounding "yes", other times, perhaps not. There are also smart and tax-efficient ways to pay down debt and "not so smart" ways – which would you prefer, more money in your pocket or a chunk of your money going one way to the IRS? It's a rhetorical question, but as the old saying goes, "failing to plan is planning to fail". There is also "plans are one thing, planning is everything."

Smart vs. not so smart? -> taking money out of your DROP to buy that RV, paying off a mortgage or other debt, buying that fancy car, toy, whatever, not to mention divorces, quadros, IRS issues, and the list goes on and on to even no reason other than they just wanted the money in their hands so to say. And, realistically you may want to or need to work a second career for a while to pay for healthcare costs or until Social Security kicks in etc. All these are addressed in your plan. The battle between "Wants and Needs" is often difficult. Can you afford to do those things without seriously risking putting a major dent in your financial security and future? We plan for them ahead of time and sometimes the answer is a resounding "yes", other times, perhaps not. There are also smart and tax-efficient ways to pay down debt and "not so smart" ways – which would you prefer, more money in your pocket or a chunk of your money going one way to the IRS? It's a rhetorical question, but as the old saying goes, "failing to plan is planning to fail". There is also "plans are one thing, planning is everything."

Do I still have your attention? If so, you may have noticed I really haven't touched upon the investment side of the equation. 457 fixed accounts may pay you 3.5% TODAY, but they are fixed (NO COLA) and may still be at 3.5% (or lower) in 10 years. Expenses aren't fixed so why should your income be? Your pension may not have a COLA, but if there were a way that your DROP and other retirement assets could have a COLA, wouldn't you want to know how?

We employ a "10% COLA/ rising income strategy" for many clients in need of current income and/or future income whereby year one you are receiving an initial 3.5% dividend, but instead of being fixed, it grows at 7-10% a year. That is a nice COLA! At this rate, the income you derive from your DROP/other retirement assets doubles every 7-10 years or so thereby helping you combat the effects of inflation and no COLA. For example, on $500,000 3.5% = $17,500 in year one or $1,458/mo. At a 10% dividend growth rate, your $17,500 initial dividend income could grow to over $34,102/yr or $2,842/mo by year 7 and so forth! Obviously, this is only one strategy and we review all these and more in person with our clients.

In summation, the lack of a COLA is not the end of the world. However, knowing how your "second half of life" financial plan and retirement future look in a "No COLA" world is vital before you retire – not 10 years into retirement. However, even those already retired should have a plan as it is never too late. Mapping a plan to address no COLA and the inflation effects over time is critical to making sure you can retire with more peace-of-mind, maybe being able to sleep better at night, and not work unless you WANT to – not because you HAVE to.

The first half was for them – the second half should be for you so you can retire one day and truly be able to say "so long tension – hello pension!" Stay safe!

About the Author

Mark Burnam is the State of Florida Financial Advisor/Director of Marketing and Client Services for The Second Half Team at C/F/R Financial LLC -- an alliance of Cross, Fernandez, and Riley CPA LLP. Proactively guiding first responders and more at 79+ departments and agencies from Ocala to South Beach better plan and prepare for retirement and their "second half of life". For more information or answers to some of your questions please email me at MBurnam@cfrcpa.com.

P.S. Previous article links are also located on our website or just email me.

Editor's Note: At the Ready exists to give a voice to responders everywhere. We believe that the information shared through At the Ready, by responders to other responders, benefits the entire responder community. We know too that information shared by others can be just as useful. In the case of this article series, the information shared will help the responder community be more prepared for the day when you turn in your badge and gun, or take-off and hang-up the turn-out gear for the last time. We asked Mark Burnam, State of Florida Financial Advisor/Director of Marketing and Client Services for "The Second Half Team" at C/F/R Financial LLC, to write about strategies you can take to ensure more peace-of-mind when that day comes.

When you retire and begin your "second half of life", work because you want to, not because you have to. Isn't that what you want? In our previous articles, we talked about the four basic steps to securing a more sound retirement, including decisions for workers 5 to 8 years out, and issues for those in already in DROP and close to actual retirement. In this article we wish to touch upon the effect of inflation in regard to one's pension income with or without a Cost of Living Adjustment (COLA).

When you retire your pension income will either be fixed or have an annual "cost of living adjustment" more commonly known as a COLA. They come in many forms from 1% - 3% a year for life, to staggered, to vanishing after a certain amount of years, to none at all. Most of the folks we work with in the Florida Retirement System (FRS) are enjoying a 3% COLA and we are now seeing a slightly reduced COLA i.e. 2.85% 2.65% and so forth for those retiring in the next few years. Their reduced COLA calculation depends upon length of service, when they entered DROP, retired, and so forth. The folks we work with in various city pension plans are all over the map in regard to COLA's as some have them and others have had their COLA's reduced or completely eliminated. It is what it is.

In our previous articles we had a DROP retiree retiring with an income of $7,000/mo(or $84,000/yr.), a DROP account of $400,000, and a 457 deferred comp plan value of $150,000. Let's take a look at two different pensioners: one with a 3% COLA and one with 0% COLA and the effects of inflation and no COLA:

Bottom line, with most of our first responders retiring in their mid-50's (give or take) coupled with longer life expectancies, you can see the devastating effects inflation can have on ones purchasing power over time. So what is one to do?

Let's also take a look at one's annual living expenses. If you had an $84,000/yr pension and your annual living expenses were $50,000 when you retired -> in year 10 your pension is still $84,000, but your expenses grew at 3% a year and are now $67,195 in real terms and in 20 years they will be $90,304! You're under water and this just assumes 3%. Healthcare, college costs, and more are all growing 5 - 7%/year, or more. Gulp!

So how does this all translate to you now? Fact: you may need to start withdrawing moneys from your DROP/other retirement accounts to fund your retirement. How much? When? For how long? Can you afford to invest all your moneys in some guaranteed fixed 3.5% rate account? Can you afford to earn only 5%? Other? Will you risk depleting your DROP/other retirement accounts with that approach at some point in your life? If so, what then?

We sometimes tend to see what is right in front of us and some folks we meet with just shrug and hope things will work out down the road. In our practice, we don't want to "wing it" with your "second half of life" financial future and just "hope things work out" for you. We want any surprises in retirement to be positive surprises so we plan accordingly. How? We "stress test" your plan by running assumptions with conservative/understated investment returns and beefed up/rainy day expenses rising at more than 3%. If your plan looks good under those conditions then you should be in great shape. If not, then it will show up under the investment return you actually need on your DROP and other assets to ensure you don't deplete these assets. Is it 3%? 5%? 7%? 9%? More? The lower return you need to earn on those assets the more options you have and the more conservative you can be. Your jobs were stressful enough all those years; do you really want to HAVE to earn over 9% a year to fund your retirement expenses and to NOT deplete your assets? Clearly not.

No Worries Plan

And the lack of a COLA is not necessarily always the biggest culprit. Sometimes it is you! It doesn't have to be, but we all know people who have blown their DROP by taking pre-mature distributions (withdrawals) without any thought or concern to the tax implications or future needs. They (or their "advisor") didn't know or give proper guidance in respect to which accounts and assets to withdraw from first. Pre-50, 55, and 59 ½ rules are important considerations and working with someone who knows these rules is a must.

Big Worries

Do I still have your attention? If so, you may have noticed I really haven't touched upon the investment side of the equation. 457 fixed accounts may pay you 3.5% TODAY, but they are fixed (NO COLA) and may still be at 3.5% (or lower) in 10 years. Expenses aren't fixed so why should your income be? Your pension may not have a COLA, but if there were a way that your DROP and other retirement assets could have a COLA, wouldn't you want to know how?

We employ a "10% COLA/ rising income strategy" for many clients in need of current income and/or future income whereby year one you are receiving an initial 3.5% dividend, but instead of being fixed, it grows at 7-10% a year. That is a nice COLA! At this rate, the income you derive from your DROP/other retirement assets doubles every 7-10 years or so thereby helping you combat the effects of inflation and no COLA. For example, on $500,000 3.5% = $17,500 in year one or $1,458/mo. At a 10% dividend growth rate, your $17,500 initial dividend income could grow to over $34,102/yr or $2,842/mo by year 7 and so forth! Obviously, this is only one strategy and we review all these and more in person with our clients.

In summation, the lack of a COLA is not the end of the world. However, knowing how your "second half of life" financial plan and retirement future look in a "No COLA" world is vital before you retire – not 10 years into retirement. However, even those already retired should have a plan as it is never too late. Mapping a plan to address no COLA and the inflation effects over time is critical to making sure you can retire with more peace-of-mind, maybe being able to sleep better at night, and not work unless you WANT to – not because you HAVE to.

The first half was for them – the second half should be for you so you can retire one day and truly be able to say "so long tension – hello pension!" Stay safe!

About the Author

Mark Burnam is the State of Florida Financial Advisor/Director of Marketing and Client Services for The Second Half Team at C/F/R Financial LLC -- an alliance of Cross, Fernandez, and Riley CPA LLP. Proactively guiding first responders and more at 79+ departments and agencies from Ocala to South Beach better plan and prepare for retirement and their "second half of life". For more information or answers to some of your questions please email me at MBurnam@cfrcpa.com.

P.S. Previous article links are also located on our website or just email me.

Editor's Note: At the Ready exists to give a voice to responders everywhere. We believe that the information shared through At the Ready, by responders to other responders, benefits the entire responder community. We know too that information shared by others can be just as useful. In the case of this article series, the information shared will help the responder community be more prepared for the day when you turn in your badge and gun, or take-off and hang-up the turn-out gear for the last time. We asked Mark Burnam, State of Florida Financial Advisor/Director of Marketing and Client Services for "The Second Half Team" at C/F/R Financial LLC, to write about strategies you can take to ensure more peace-of-mind when that day comes.